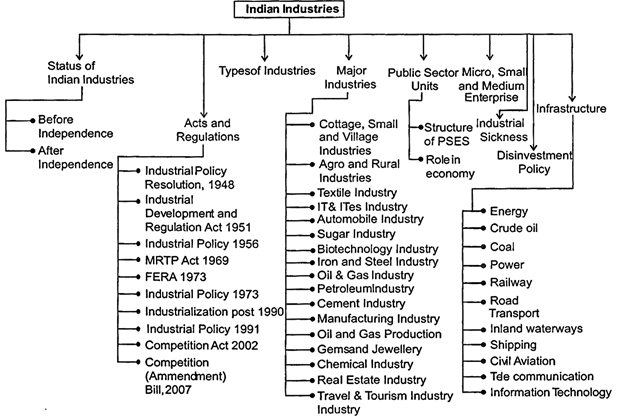

Industries and Infrastructure

Category : UPSC

Industries and Infrastructure

Introduction

Growth of industries has been always focus area of the government. The reason behind this is die important role played by the industries in Gross Domestic Product (GDP) of India. The government, therefore, has many schemes and incentives to facilitate growth and development of industries. It has been generally noticed that most of the developing countries gradually move from the predominance of agriculture towards that of industries in economy as they progress on the path of economic development.

Indian economy, however portrays a contradictory trend. Here, the economic has by passed industries growth to rapid growth of services sector. The rapid growth of services may be largely attributed to reform and liberalisation of the 1990s. Indian industries contribute 18% of India's GDP and employ about 19% of work force. Major industries of our country are textiles, chemicals, food processing, steel, cement, petroleum, pharmaceuticals, etc.

STATUS OF INDIAN INDUSTRIES

Before Independence

Pre-British India was a major manufacturing country. India in 1750 supplied nearly a quarter of world production of manufactured goods, thus attracted traders from different parts of Asia. Hundred years later, the situation turned altogether different. Industries in India were in disarray.

India witnessed a phase of rapid de-industrialisation under the colonial rule. Destruction of traditional industries was not ac-companied with foundation of modern industries.

It was only in the middle of the 19th century the modern industries began to be established in India. Even when it started the process was painfully slow.

The British investors built a railway system in the second half of 19th century. Besides the railways the large scale industries were confined to the plantations and a few consumer goods industries like textiles. There was limited development of mining like coal and iron. The ownership of these industries except textile was predominantly European and mostly British.

There was almost complete absence of heavy or capital goods industries. The first steel in India was produced only in 1913.

Thus India lacked such basic industries as steel, metallurgy, machine, chemical and oil. India also lagged behind in the development of electric power.

Industrial Growth after Independence

Prior to independence the ownership or control of much of the large private industries were in the hands of managing agencies, which grew under the British system and had access to London money markets. Thus the owners of these managing agencies controlled a major portion of the economy, prior to independence.

But things changed after independence. Parliament enacted a legislation to curb the powers of managing agencies. By 1971 the government had banned the managing agencies.

The Industrial Policy Resolution, 1948, clearly put forward the goal of the Government's policy with respect to industrialization. This was the first economic policy of our country. It declared that India would be a mixed economy.

Following are the major highlights of this resolution.

· Those industries completely owned by the Government e.g. ordinance, atomic energy, railways and any industry of national importance were to be the exclusive domain of the Central government. Certain important industries like coal, iron and steel, aircraft manufacture, ship building, telephone, telegraphs and communications, were given the permission to operate for ten years, at the end of which the government would nationalize them.

· A group of 18 specified industries (of medium category) were in control of the state governments in liaison with the Central government.

· The remaining industrial options which were not covered by either the centre or state lists, were left open to the private sector.

· This policy was to be reviewed after 10 years.

Industrial Development and Regulation Act 1951

The Act gave complete authority to the Government. This resulted in the bureaucracy extending complete control over the industrialization of the country.

· They controlled the authorization of capability, where about and growth of any request for manufacture of new products.

· They controlled the authorization of foreign exchange expenditure on the import of plant and machinery.

· They controlled the authorization for the terms of international joint ventures.

Industrial Policy In 1956

In 1956 a new policy for industrialization was initiated.

· All basic and sensitive industries in India were under the purview of public sector undertakings (PSUs) and were called as schedule. A industries. The Centre had complete monopoly over these industries. The then PM Pandit Jawaharlal Nehru termed the PSUs the ?temples of modern India? in this industrial policy. In this category 17 industries were included. Out of these arms and ammunition, atomic energy, rail transport and air transport were to be government monopolies. For the rest 13 industries, new units were to be established only in public sector, but the existing private sector units were allowed.

· ?Schedule B? was a mixed sector of public and private enterprises. While private participation was not denied, the government policy was to increase the participation of public sector units in these industrial sectors. 12 industrial sectors were put under this category. This category also carried the provision of compulsory licensing. This provision led to the establishment of the so called ?Licence- Quota- Permit raj? in the economy.

· The remaining industries came under Schedule C, to be under the control of private initiative.

· The policy of 1956, for the first time, recognized the contribution of small scale industries in the growth of the Indian economy. It laid stress on rational distribution of national income and effective utilization of resources.

· This policy is considered one of the most important industrial policies of India as it decided the nature and scope of the Indian economy till the reforms of 1991.

MRTP Act-1969

The Government of India appointed a Monopolies Inquiry

Commission, in 1964 under Justice K. C. Dasgupta, to study the presence and outcomes of concentration of economic power in private sector. The Commission observed the presence of monopolistic and restrictive practices in certain key sectors of the economy. The Commission recommended the setting up of the Monopolies and Restrictive Trade Practices Commission and this eventually resulted in the MRTP Act in 1969.

FERA 1973

The Foreign Exchange and Regulation Act (FERA) was passed in 1973. This resulted in a tremendous shift in the foreign investment policy of the Government of India.

Foreign Investment was allowed in only those industries that were directly into exports.

Restrictions were placed on foreign investments. International companies could hold a maximum of 40% equity. But some industries in the field of advanced technology were given permission for 51% foreign capital. This has often been called a draconian act which hampered the modernization and growth of Indian industries.

Industrialization Post 1990

· Exemption from licensing was allowed for all startups and for those with an investment worth Rs 2.5 crores in fixed assets and a right to import up to 30 % of the total value of plant and machinery.

· Foreign equity investment was allowed up to 40%.

· Geographical restrictions and investment cap for small industries were removed.

At the time of liberalization the Indian industries were not competitive in the global scenario. They could not face the stiff competition from the foreign industries; hence many industries sold their companies to multinational corporations or entered into joint ventures with foreign companies or shut down the business.

At the same time a new wave of service industries emerged, which positioned itself in the outsourcing segment. IT and ITE?s industries flourished providing employment to millions of graduates.

Industrial Policy 1991-[Period of Economic

Reforms]

(A) Objectives

· To maintain a sustained growth in productivity.

· To enhance gainful employment.

· To achieve optimum utilisation of human resources.

· To attain international competitiveness.

· To transform India into a major partner and players in the global arena.

(B) Main Focus on

(C) Policy Measures

(i) Liberalisation of Industrial Licensing Policy.

(ii) Introduction of Industrial Entrepreneur?s Memorandum (i.e. no industrial approval is required for industries not requiring compulsory licensing).

(iii) Liberalisation of Locational Policy.

(iv) Liberalised policy for Small Scale Sectors.

(v) Non-Resident Indians Scheme (NRIs are allowed to invest upto 100% equity on non-repatriation basis in all activities except for a small negative list).

(vi) Electronic Hardware Technology Park (EHTP), Software Technology Park (STP) Scheme for building up strong electronic industry to enhance exports.

(vii) Liberalised policy for Foreign Direct Investment (FDI).

(viii) Abolition of the MRTP limit.

(ix) FERA was replaced by highly liberal FEMA.

Leading: Liberalisation

Liberalisation is a relaxation of Government restrictions, usually in areas of social, political and economic policy. It is commonly known as free trade. It implies removal of restrictions & barriers to free trade.

1. Privatization: Privatization can be denned as the transfer of ownership arena & control of public sector units to private individuals or companies.

2. GSobalization: It refers to a process whereby there are social, cultural, technological exchanges across the border.

Competition Act, 2002

In the present era of LPG (Liberalisation, Privatisation and Globalisation), it was felt that the existing Monopolies and Restrictive Trade Practices Act. 1969 has become hurdle in certain respects and there is a need to shift our focus from curbing monopolies to promoting competition. Hence a new law, the Competition Act has been enacted and published in the gazette of India on January 14, 2003 for bringing competition in the Indian market. The main objectives of the Act are to establish a commission to prevent practices having adverse effect on competition, to promote and sustain competition in markets in India, to protect the interests of consumers and to ensure freedom of trade carried on by participants in market in India and for related matters.

The Act mainly covers the following aspects:

(i) Prohibition of anti-competitive agreements;

(ii) Prohibition of abuse of dominance;

(iii) Regulation of combination (acquisitions, mergers and amalgamations of certain size);

(iv) Establishment of Competition Commission of India (CCI): and

(v) Functions and powers of CCl.

The Act is expected to curb those practices, which would have an adverse effect on competition.

Competition [Amendment) Act, 2007

On September 10, 2007 Parliament finally passed the long pending Competition (Amendment) Bill, 2007 that empowers the Competition Commission of India (CCI) to act as the competition regulator and to deal with a host of contemporary economic issues including monopolies and take-overs of corporate firms.

According to the Bill's provisions, the CCI replaced Monopolies and Restrictive Trade Practice Commission (MRTPC). The CCI was established in 2003. Under new provisions, the MRTPC continued for two years after the Constitution of CCI for dealing with pending cases but after two years MRTPC was dissolved.

However, MRTPC could not entertain any new cases after the CCI was constituted. Cases pending with MRTPC after two years of setting up of CCI were transferred to the latter.

Industries Enterprises

Enterprises have been categorized broadly into those engaged in (i) manufacturing and (ii) providing/ rendering of services. Both categories have been further classified into micro, small and medium enterprises, based on their investment in plant and machinery (for manufacturing enterprises) or in equipment (in case of enterprises providing or rendering services) as under:

The following are the investment requirements under the

Manufacturing Enterprises category:

Micro Enterprises are those enterprises which have investment upto Rs. 25 lakh. Small Enterprises are those enterprises with investment above 25 lakh and upto 5 crore.

Medium Enterprises are those enterprises which have investment above T 5 crore and upto ?10 crore. The following are the investment requirements under the

Service Enterprises category:

Micro Enterprises investment includes companies with investment upto Rs. 10 lakh. Small Enterprises need an investment above 10 lakh and upto 2 crore. Medium Enterprises are those enterprises which have an investment above 2 crore and upto 5 crore.

Small and Medium Enterprises Development Bill 2005 (which was introduced in the Parliament on May 12, 2005) was approved by the President and became an Act. This Act, named as ?Small and Medium Enterprise Development Act, 2006? became effective from October 2, 2006. This Act makes a different category for medium level enterprises.

There are 8 core industries in the economy coal, crude oil,

Natural Gas, Petroleum Refinery Production, Fertilizers, Steel, Cement and Electricity.

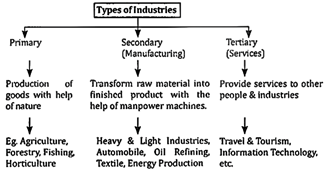

MAJOR INDUSTARISE

Major Cottage, Small and Village Industries

In a broad sense cottage, small and village industries are treated similar but they fundamentally differ from each other.

Cottage industry is run by family members on full or part time basis. It possesses negligible capital investment. The production is done by hands and no wage earning person is employed in cottage industry.

Small industrial units employ wage earning labour and production is done by the use of modern techniques. Capital investment is also present in small industries. A few cottage industries which are export-oriented have been included in the category of small sector so that facilities provided to small units may also be given to export-oriented cottage industries.

The industries established in rural areas having population below 10,000 and having less than `15,000 as fixed capital investment per worker will be termed as village industries.

KVIC and state village Industries Board provide economic and technical assistance in establishing and operating these industrial units.

Agro and Rural Industries

Development of agro and rural industries based on local raw materials, skills and technology has been identified as one of the most important activities for gainful employment in the rural non-farm sector and for overall growth of the national economy. Various policies and programmes are being implemented by the Government through Khadi and Village Industries Commission (KVIC) and Coir Board and Prime Minister's Rozgar Yojana (PMRY) with the active co-operation and participation by RBI, other banks and the state governments for the promotion of agro and rural industries in rural areas and small towns.

For the development of Khadi and Village Industries (KVI)

Sector, the Government is implementing various programmes schemes through KVIC, Textile Industry in India India?s textiles sector is one of the oldest industries in Indian economy dating back several centuries. Even today, textiles sector is one of the largest contributors to India?s exports. India is the world's second largest exporter of textiles and clothing contributing approximately 12% of total exports.

The Indian textiles industry, currently estimated at around US![]() 108 billion, is expected to reach US

108 billion, is expected to reach US![]() 223 billion by 2021.

223 billion by 2021.

The textile industry contributes to 10% of manufacturing production, 2% of India?s GDP and to 13% of the country's export earnings. With over 45 million people employed directly, textile industry is one of the largest source of employment generation in the country. Readymade garments are the largest contributor to total textile and apparel exports from India in FY15. The segment had a share of 40%, in overall textile exports. Cotton and handmade textiles were also major contributors with shares of 31% and 16%, respectively.

The textile and apparels industry is broadly classified into the following segments:

History of Textiles Industry

Indian textiles industry has its own history in the world.

MALMAL of Dhaka? was famous all over the world.

· The first Indian modernised cotton mill, located in Kolkata in 1818, was not successful. The second mill named ?Bombay Spinning and Weaving Co? was established in 1854 at Bombay by KGN Daber. Truly speaking, this mill only laid the foundation stone of modern cotton industry in India.

· Since 1854, the number of cotton mills has been rapidly increasing.

· Development of cotton industry had a great role in Indian freedom struggle. Various movements like Non-Cooperation Movement, Quit India Movement, etc. created a wave of boycotting foreign goods and accepting swadeshi goods, which helped a lot in developing indigenous industries.

· The partition of India adversely affected the Indian cotton industry. Most of the muslim weavers migrated to Pakistan and this industry got divided into two parts.

· There were 394 cotton mills in India before the partition.

· Out of these, 14 mills went to Pakistan and the remaining 380 cotton mills continued to operate in India.

· On the other hand, 40% of cotton producing area became the part of Pakistan and only 60% area was transferred to India.

· So after independence India had to import raw material to meet the input requirements of 380 cotton mills.

· India?s Five Year Plans proved a boon to cotton industry, as this industry not only made remarkable development but also established itself in international markets.

· The Government by its Textile Development and Regulation Order 1993 has made mis industry licence-free.

· The textile industry is concentrated mainly in the states of Maharashtra, Tamil Nadu and Gujarat.

IT & ITeS Industry in India

India is the world?s largest sourcing destination for the information technology (IT) industry, accounting for approximately 67% of the USS 124-130 billion market.

India?s IT industry amounts to 12.3% of the global market, largely due to exports. Export of IT services accounted for

56.12%, of total IT exports (including hardware) from India.

The Business Process Management (BPM) segment accounted for 23.46% of total IT exports during FY15.

The IT industry has also created significant demand in the Indian education sector, especially for engineering and computer science.

The Indian Information Technology (IT) sector is expected to grow 11 % per annum and triple its current annual revenue to reach US![]() 151.6 billion) by 2018, accounting for 5% of me country?s gross domestic product (GDP), according to a report by the Boston Consulting Group (BCG) and Internet and Mobile Association of India

151.6 billion) by 2018, accounting for 5% of me country?s gross domestic product (GDP), according to a report by the Boston Consulting Group (BCG) and Internet and Mobile Association of India

(IAMAI). India?s internet user base reached over 350 million by June 2015, the third largest in the world, while the number of social media users grew to 143 million by April 2015 and smartphones grew to 160 million.

Indian start-ups are expected to receive funding worth US![]() 550 billion to US

550 billion to US![]() 1 trillion by 2025, as per research firm McKinsey.

1 trillion by 2025, as per research firm McKinsey.

SMAC, increasing at a CAGR of approximately 30% to around US![]() 650-700 billion by 2020. The social media is the second most lucrative segment for IT firms, offering a US

650-700 billion by 2020. The social media is the second most lucrative segment for IT firms, offering a US![]() 250 billion market opportunity by 2020.

250 billion market opportunity by 2020.

The Indian e-commerce segment is US![]() 12 billion in size and is witnessing strong growth and thereby offers another attractive avenue for IT companies to develop products and services to cater to the high growth consumer segment.

12 billion in size and is witnessing strong growth and thereby offers another attractive avenue for IT companies to develop products and services to cater to the high growth consumer segment.

Indian Autombile Industry

The Indian automobile industry registered a growth of 8.68% in the FY 2014 - 15 over last year and produced 23.37 million vehicles. The automobile industry accounts for 7.1% of the country?s gross domestic product (GDP).

Two-wheeler production is projected to rise from 18.5 million in FY15 to 34 million by FY20. Furthermore, passenger vehicle production is expected to increase to 10 million in FY20 from 3.2 million in FY15.

The government aims to develop India as a global manufacturing as well as a research and development (R&D) hub. It has set up National Automotive Testing and R&D Infrastructure Project (NATRIP) centres as well as a National Automotive Board to act as facilitator between the government and the industry.

Alternative fuel has the potential to provide for the country?s energy demand in the auto sector as the CNG distribution network in India is expected to rise to 250 cities in 2018 from 125 cities in 2014.

Furthermore, die luxury car market can register high growth and is expected to reach 150,000 units by 2020.

Sugar Industry

Sugar industry occupies an important place among agriculture based industries. Sugar industry is the second, largest industn? after cotton textile industry among agro based industries- of the country. This industry provides not only employment to a substantial number of persons but also holds the potentialities of developing other industries related to its by-products.

India is the largest consumer of sugar and the second largest producer of sugar with a share of over 15% of world sugar production. The importance of sugar industry in India can be estimated from the fact that about 45 million sugarcane growers and a large number of rural labourers depend on sugarcane and sugar industry for their livelihood. Sugar cultivation accounts for 3% of total cultivated area and contributes 7.5%1 of the gross value of agricultural production.

The industry also benefits the nearly 2.5 crore people who grow sugarcane in India. In India, the major sugar producing states are Maharashtra, Gujarat, Uttar Pradesh, Haryana, Tamil Nadu, Punjab, Karnataka, Bihar and Andhra Pradesh.

The Central Government fixes the Statutory Minimum Price (SMP) of sugarcane for each sugar season. The SMP is fixed on the basis of the recommendations of the Commission for Agricultural Cost and Prices (CACP) and after consulting the State Governments and associations of sugar industry and cane growers.

In 2012 Rangrajan Committee w'as set up the PMO to recommend on issues relating to the decontrol of the sugar sector.

The Rangrajan Committee had suggested removal of levy obligations for sugal mills. It also suggested giving freedom to mills to sell sugar in the open market, and introducing a stable export and import policy.

Government accepted some of these recommendations. In 2013 the government removed the levy obligation and oblished the quarterly release mechanism and the restrictions on quantity of sugar released for open market sale, giving mills greater flexibility in managing cash flows.

Biotechnology Industry in India India is among the top 12 biotech destinations in the world and ranks third in the Asia-Pacific region.

The Indian biotech industry holds about 2% share of the global biotech industry. The Indian biotechnology sector is expected to grow from the current US![]() 100 billion by 2025, growing at an average rate of 30%.

100 billion by 2025, growing at an average rate of 30%.

Biopharma is the largest sector contributing about 64% of the total revenue followed by bioser vices (18%), bioagri (14%), bioindustry (3%), and bioinformatics contributing (1%).

The high demand for different biotech products has also opened up scope for the foreign companies to set up base in India. India has emerged as a leading destination for clinical trials, contract research and manufacturing activities owing to the growth in the bioservices sector.

India has all the ingredients to become a global leader in affordable healthcare. If there is an annual investment of US![]() 4.01 billion to USS 5.02 billion in the next five years, the biotech industry can grow to US

4.01 billion to USS 5.02 billion in the next five years, the biotech industry can grow to US![]() 100 billion by 2025, with a 25% return on investment, and set a growth rate of 30% year-on-year.

100 billion by 2025, with a 25% return on investment, and set a growth rate of 30% year-on-year.

Iron and Steel Industry

The advent of Iron and Steel Industry took place in India in the year 1870 when Bengal Iron Works Company established its plant at Kulti near Jharia, West Bengal. This plant produced only cast iron. Large scale iron and steel plant was started in 1907 by TISCO established at Jamshedpur.

In 1919, Indian Iron and Steel Company (IISCO) was established at Burnpur. Both TISCO and IISCO are private sector companies. The first public sector company was ?Vishwashwaraiya Iron and Steel Works at Bhadravat?.

After independence, though a thought was given to develop Iron and Steel Industry in First Five Year Plan, but this materialised in Second Five Year Plan. The Second Plan established three steel plants in the public sector-Bhilai (with assistance of USSR), Durgapur (with assistance of U.K.) and Rourkela (with assistance of West Germany).

All the three public sector plants started production between 1956 and 1962.

All the three public sector steel plants were expanded during Third Five Year Plan and attempts were made to establish one more public sector steel plant at Bokaro with the assistance of USSR.

Oil and Gas Industry in India

The oil and gas sector is among the six core industries in India and plays a major role in influencing decision making for all the other important sections of the economy. In 1997-98, the New Exploration Licensing Policy (NELP) was envisaged to fill the ever-increasing gap between India's gas demand and supply. The Government of India has adopted several policies to fulfil the increasing demand. The Government has allowed 100% foreign direct investment (FDI) in many segments of the sector, including natural gas, petroleum products, and refineries, among others.

Presently, domestic production accounts for more than three-quarters of the country's total gas consumption. India increasingly relies on imported LNG. The country was the fifth-largest LNG importer in 2013, accounting for 5.5% of global imports.

India?s LNG imports are forecasted to increase at a CAGR of 33% during 2012-17.

Energy consumption pattern in India

State-owned Oil and Natural Gas Corporation (ONGC) dominates the upstream segment (exploration and production), accounting for approximately 68% of the country's total oil output (FY14).

PAHAL - Direct Benefit Transfer for LPG consumer (DBTL) scheme was launched in 54 districts on November 11, 2014 and expanded to rest of the country on January 1, 2015 will cover 15.3 crore active LPG consumers of the country. 24x7 LPG service via web launched to provide LPG consumers an integrated solution to carry out all services at one place, through MyLPG.in, from the comfort of their home.

The Government of India launched the 'Give It Up' campaign on LPG subsidy that helped it save ' 140 crore (US![]() 21.11 million) as on 22nd July 2015 with nearly 12.6 lakh Indians registering for the cause.

21.11 million) as on 22nd July 2015 with nearly 12.6 lakh Indians registering for the cause.

Subsidised cooking gas will no longer be provided to consumers earning ?10 lakh or more a year from January 1, 2016.

The rule will initially be implemented on self-declaration basis for cylinders booked from January 2016 onwards.

India has proven oil reserves of 5.7 billion barrels, and gas reserves of 1.4 trillion cubic meters, yet given the low production base, the country remains a net importer of energy.

Petroleum Industry

Initially, Digboi (Assam) was the only oil producing area of the country. But now, a number of regions having oil reserves have been identified and the oil is being extracted in these regions. Oil regions in India are Assam, Tripura, Manipur, West Bengal, Mumbai, Gujarat, Jammu and Kashmir, Himachal Pradesh, Tamil Nadu, Andhra Pradesh, Rajasthan, Coastal area ofKerala and Andman & Nicobar Islands.

India has 21 refineries - 17 in the public sector, 3 in the private sector and one in joint venture. Out of 17 public sector refineries, 8 are owned by Indian Oil Corporation Ltd. (IOCL), 2 each by Chennai Petroleum Corporation Ltd. (a subsidiary of IOCL), Hindustan Petroleum Corporation Ltd. (HPCL), Bharat Petroleum Corporation Ltd. (BPCL) and Oil & Natural Gas Corporation Ltd. (ONGC). Numaligarh Refinery Limited (a subsidiary of BPCL) and Manglore Refinery and Petrol Chemicals Ltd. have one refinery each. The Joint Venture Refinery belongs to Bharat Petroleum Corporation Ltd.

Cement Industry in India

India is the second largest producer of cement in the world.

India's cement industry is a vital part of its economy, pro-viding employment to more than a million people, directly or indirectly.

Some of the recent major government initiatives such as development of 100 smart cities are expected to provide a major boost to the sector. Expecting such developments in the country and aided by suitable government foreign policies, several foreign players such as Lafarge-Holcim, Heidelberg Cement, and Vicat have invested in the country in the recent past.

India's cement demand is expected to reach 550-600 million tonnes per annum (MTPA) by 2025. The housing sector is the biggest demand driver of cement, accounting for about 67% of the total consumption in India.

In the 12th Five Year Plan, the Government of India plans to increase investment in infrastructure to the tune of US![]() 1 trillion and increase the industry?s capacity to 150 MT.

1 trillion and increase the industry?s capacity to 150 MT.

Manufacturing Industry in India

Indian Manufacturing sector currently contributes 16% to GDP (2015) and gives employment to 12% (2014) of the country?s workforce. Studies have estimated that every job created in manufacturing has a multiplier effect, creating 2-3 jobs in the services sector.

Prime Minister Mr Narendra Modi, has launched the 'Make in India? initiative to place India on the world map as a manufacturing hub to give global recognition to the Indian economy.

In a major boost to the 'Make in India' initiative, the Government of India has received investment proposals of over USS 3.05 billion till end of August 2015 from various companies.

India has become one of the most attractive destinations for investments in the manufacturing sector.

Clean energy investments in India increased to USS 7.9 billion in 2014, helping the country maintain its position as the seventh largest clean energy investor in the world.

Gems and Jewellery Industry in India

Contributor to semi-skilled employment. Consists of 3 segments - Diamonds, Gold Jewellery & Coloured Gemstones.

It is extremely export oriented and labour intensive. It contributes to 6-7% of the GDP.

The gems and jewellery sector in India is engaged in sourcing, manufacturing, and processing, which involves cutting, polishing and selling precious gemstones and metals such as diamonds, other precious stones, gold, silver and platinum.

It contributed US![]() 39.9 billion in terms of foreign exchange earnings in FY 2014-15.

39.9 billion in terms of foreign exchange earnings in FY 2014-15.

According to a report by Research and Markets, the jewellery market in India is expected to grow at a CAGR of 15.95% over the period 2014-2019.

Chemical Industry

Chemical industry is one of the oldest industries. It includes basic chemicals and its products, petrochemicals, fertilisers, paints and varnishes, gases, .soap, perfumes, toiletries and pharmaceuticals. This industry is one of the most diversified of all industrial sectors covering more than 70,000 commercial products. It not only plays a crucial role in meeting die daily needs of the common man, but also contributes significantly towards industrial and economic growth of the nation. It is an important constituent of the Indian economy. Its turnover size is estimated at around US ![]() 160 billion approx., which is equivalent to about 3% of India's GDP. Major chemicals undergo several stages of processing to be converted into downstream chemicals. These processed chemicals are used in agriculture and industry as auxiliary materials such as adhesives, unprocessed plastics, dyes and fertilizers.

160 billion approx., which is equivalent to about 3% of India's GDP. Major chemicals undergo several stages of processing to be converted into downstream chemicals. These processed chemicals are used in agriculture and industry as auxiliary materials such as adhesives, unprocessed plastics, dyes and fertilizers.

Chemicals are also directly used by consumers in the form of pharmaceuticals, cosmetics, household products, paints, etc.

Alkali chemicals, inorganic chemicals and organic chemicals constitute the major segments of the chemicals industry.

Real Estate Industry in India

India is the second largest employer of Real estate after agriculture and is slated to grow at 30% over the next decade.

The real estate sector comprises four sub sectors - housing, retail, hospitality, and commercial.

Bengaluru is expected to be the most favoured property investment destination for NRIs, followed by Ahmedabad, Pune, Chennai, Goa, Delhi and Dehradun.

The Indian real estate market is expected to touch US![]() 180 billion by 2020. The housing sector alone contributes 5-6% to the country?s Gross Domestic Product (GDP).

180 billion by 2020. The housing sector alone contributes 5-6% to the country?s Gross Domestic Product (GDP).

Mumbai is the best city in India for commercial real estate investment, with returns of 12-19% likely in the next five years, followed, by Bengaluru and Delhi-National Capital Region (NCR).

Under the Sardar Patel Urban Housing Mission. 30 million houses will be built in India by 2022, mostly for the economically weaker sections and low-income groups, through public-private-partnership (PPP) and interest subsidy.

TraveS & Tosisrism Industry

According to World Economic Forum's Travel & Tourism

Competitiveness Report 2015, India ranks 52nd globally out of 141 economies ranked on Travel & Tourism Competitiveness Index. Tourism in India accounts for 6.8% of the GDP & is the 3rd largest foreign exchange earner for the country. The direct contribution of Tourism & Hospitality sector to GDP totaled US ![]() 44.2 billion in 2015. Over 7.757 million foreign tourist arrivals were reported in 2015. Important Travel Companies in India Cox Kings Ltd., India Tourism Development Corporation Ltd., Thomas Cook Ltd.

44.2 billion in 2015. Over 7.757 million foreign tourist arrivals were reported in 2015. Important Travel Companies in India Cox Kings Ltd., India Tourism Development Corporation Ltd., Thomas Cook Ltd.

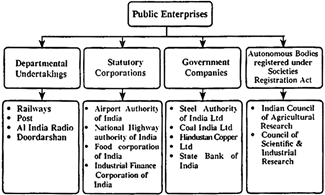

PUBLIC SECTOR UNITS

Most countries, including India, have adopted a mixed economy model that encourages the role of the public as well as private sector enterprises. Since Independence, the Indian government made sustained efforts to bring about balanced development by setting up public sector enterprises (PSEs). The role of the PSEs was earlier limited to basic, heavy and core industries, which were considered of strategic importance and vital for mass consumption. Furthermore, the government had to step in and set up these huge PSEs because the nation was in the initial stages of development and private enterprises could not afford massive investments which the core sector called for. In later years, PSEs have penetrated into production of essential consumer goods and have begun to spread into wide areas of the economy including non-infrastructure and other non-core areas.

· The public sector banks (PSBs), which have played an important role in shaping up the Indian economy since the pre-independence period until now, continue to dominate the Indian banking industry, accounting for more than 70% share of total banking business in India.

· With the introduction of economic reforms and liberalisa-tion in 1991, the Government initiated a systemic shift to a more open economy with greater reliance on market forces and a larger role of the private sector, including foreign investment.

· The PSEs were exposed to competition from domestic private sector companies as well as foreign MNCs. To sustain in a growing competitive scenario, PSEs have undertaken several steps to perform and operate on par with their private peers such as adopting state-of-the-art technology, focusing on improving productivity, giving performance-related pay, offering additional welfare facilities and other benefits to employees, establishing brands and increasing marketing efforts.

Structure of PSEs in India

The PSEs in India are basically categorised under four broad types based on their ownership structure. These include:

(i) Departmental undertakings,

(ii) Statutory corporations,

(iii) government-owned companies and

(iv) Autonomous bodies set up as registered societies.

(i) Departmental undertakings

Departmental undertakings are primarily meant to provide essential services such as railways. They function under the control of the respective ministries of Government of India (GOI). A departmental undertaking structure is considered suitable for activities the government aims to keep in its control in view of the public interest.

(ii) Statutory corporations

Statutory corporations are public enterprises that came into existence by a Special Act of the Parliament. The Act defines the powers and functions, rules and regulations governing the employees and the relationship of the corporation with government departments.

(iii) Government-owned companies

Government-owned or controlled companies refer to companies in which 51 % or more of the paid up capital is held by the Central or any state government (partly or wholly by both). It is registered under the Indian Companies Act and is fully governed by the provisions of this Act.

(iv) Autonomous bodies

Autonomous bodies are set up whenever it is felt that certain functions need to be discharged outside the governmental set up with some amount of independence and flexibility without day-to-day interference from the governmental machinery. These bodies are set up by the concerned ministries or their departments and are funded through grants-in-aid, either fully or partially, depending on the extent which such institutes generate internal resources of their own. These grants are regulated by the Ministry of Finance (MOF) through their instructions. They are mostly registered as societies under the ?Societies Registration Act? and in certain cases they have been set up as statutory institutions under the provisions contained in various Acts.

CPSE's Role in Economy

· CPSE investments have a multiplier effect on the economy

During the first five-year plan (1950-51 to 1955-

56) There were only 5 CPSEs with a total financial investment (Including equity plus long-term loans) of Rs. 290 million, whereas at present, in 2017, there are as many as 290 CPSEs, wherein, 169 are Holding CPSEs and 121 are the subsidiaries. There are around 13.51 lakh employees, excluding contractual workers in these 290 CPSEs. As of Mar 31, 2012, the total financial investment of CPSEs was 7,292.3 billion, showing a CAGR of around 12% during the same period.

· CPSEs continue to dominate domestic output of key sectors

CPSEs continue to hold control across several industries, despite opening up of several sectors for private investment.

CPSEs continue to have complete monopoly in nuclear power generation. Other leading areas of dominance are coal (over 80%), crude oil (over 70%), refineries (over 55%) and wired lines (over 80%). However, their share has decreased considerably, with the exception of coking coal and power generation.

Corporations & Government companies are divided into three categories - Maharatna, Navratna and Miniratna. As on 26th October 2014 there are 7 Maharatna, 17 Navratna & 73 Miniratna.

Maharatna

Criteria for grant of Maharatna status:

The CPSEs fulfilling the following criteria are eligible to be considered for grant of Maharatna status.

(i) Having Navratna status.

(ii) Listed on Indian stock exchange with minimum prescribed public shareholding under SEBI regulations.

(iii) Average annual turnover of more than Rs. 25,000 crore, during the last 3 years.

(iv) Average annual net worth of more than Rs.15,000 crore, during the last 3 years.

(v) Average annual net profit after tax of more than Rs.5,000 crore, during the last 3 years.

(vi) Should have significant global presence/international operations.

Companies:

1. Bharat Heavy Electricals Limited

2. Coal India Limited

3. GAIL (India) Limited

4. Indian Oil Corporation Limited

5. NTPC Limited

6. Oil & Natural Gas Corporation (ONGC) Limited

7. Steel Authority of India Limited

Navratna

Criteria for grant of Navratna status:

The Miniratna Category - I and Schedule ?A? CPSEs, which have obtained ?excellent? or ?very good? rating under the Memorandum of Understanding system in three of the last five years, and have composite score of 60 or above in the six selected performance parameters, namely,

(i) net profit to net worth,

(ii) manpower cost to total cost of production/services,

(iii) profit before depreciation, interest and taxes to capital employed,

(iv) profit before interest and taxes to turnover,

(v) earning per share and

(vi) Inter-sectoral performance.

Companies:

1. Bharat Electronics Limited

2 Bharat Petroleum Corporation Limited

3. Container Corporation of India Limited

4. Engineers India Limited

5. Hindustan Aeronautics Limited

6. Hindustan Petroleum Corporation Limited

7. Mahanagar Telephone Nigam Limited

8. National Aluminium Company Limited

9. National Buildings Construction Corporation Limited

10. NMDC Limited

11. Neyveli Lignite Corporation Limited

12. Oil India limited.

13. Power Finance Corporation Limited

14. Power Grid Corporation of India Limited

15. Rashtriya Ispat Nigam Limited

16. Rural Electrification Corporation Limited

17. Shipping Corporation of India Limited

Mini-ratna ? I

Upto 500 crore or equal te net worth (whichever is lower) Mini-ratna - II

Upto 300 crore or upto 50% of net worth (whichever is lower)

MICRO, SMALL AND MEDIUM ENTERPRIS-

ES IN INDIA

As per the MSME (Development) Act, 2006 micro, small and medium enterprises are defined on the basis of the level of investment in plant and machinery for manufacturing units and on equipment in service sector units.

|

Classification |

Manufacturing |

Service |

|

Micro |

Rs. 25 lakh |

Rs. 10 lakh |

|

Small |

Rs. 5 crore |

Rs.2 crore |

|

Medium |

Rs. 10 crore |

Rs.5 crore |

SIGNIFICANCE

Small scale industries (SSI) are production units with a capital investment of up to Rs. one crore.

· It plays a vital role in the growth of India. It contributes almost 40 % of the gross industrial value added in the Indian economy, 6% of GDP and 35% of exports.

· It has been estimated that a million rupees of investment in fixed assets in the small scale sector produces 4.62 million worth of goods or services. The small scale sector in India is very diverse producing 8000 products from traditional handicraft to high end technical instruments.

· The small-scale sector has grown rapidly over the years.

· The growth rates during the various plan periods have been very impressive.

· When the performance of this sector is viewed against the growth in the manufacturing and the industry sector as a whole, it instils confidence in the resilience of the small scale sector.

Employment

· MSME Sector in India creates largest employment

opportunities for the Indian populace, next only

to Agriculture. It has been estimated that 100,000

rupees of investment in fixed assets in the small-

scale sector generates employment for four

persons.

· Food products industry has ranked first in generating employment, providing employment to 0.48 million persons (13.1%). The next two industry groups were Non-metallic mineral products with employment of 0.45 million persons (12.2%) and Metal products with 0.37 million persons (10.2%).

· In chemicals and chemical products, machinery parts except electrical parts, wood products, basic metal industries, paper products and printing, hosiery and garments, repair services and rubber & plastic products, the contribution ranged from 9 % to 5 %, the total contribution by these eight industry groups being 49%.

· In all other industries the contribution was less than 5%.

· MSME Sector plays a major role in India's present export performance. 45%-50% of the Indian Exports is contributed by MSME Sector. Direct exports from the MSME Sector account for nearly 35% of total exports. Besides direct exports, it is estimated that small-scale industrial units contribute around 15% to exports indirectly. This takes place through merchant exporters, trading houses and export houses. They may also be in the form of export orders from large units or the production of parts and components for use or finished exportable goods.

INDUSTRIAL SICKNESS

Industrial Sickness refers to the situation where an industrial firm performs poorly, incurs losses for many years and defaults in its repayment obligations.

RBI defines a sick unit as ?One which has incurred a cash loss for one year and likely to continue incurring losses in the following year. The unit which has an in balance in its financial structure such as current ratio is less than 1:1 and there is worse trend in debt equity ratio.

Industrial sickness can be caused by internal and external factors.

· Internal factors could be mismanagement, lack of finance wrong dividend policy, not providing for reserves or deliberate ?milking? of the unit by the owners.

· External factors could be wrong government policy, power shortage, non-availability of raw materials, transport problem, lack of technological advancement and labour disputes.

Since 1987, the entire responsibility to tackle sickness was entrusted to the quasi-judicial body set up for the purpose, i.e. the Board/or Industrial and Financial Reconstruction (BIER).

The BIFR approves and sanctions rehabilitation schemes for sick companies that are referred to it. The functioning of BIFR, however, has been criticised over the years because of the adoption of time consuming procedures which lead to delays in rehabilitation.

The government set up the Justice Eradi committee to recommend a mechanism for revival as well as closure of a sick unit. On the recommendations of the panel, the government has decided to set up a National Company law Tribunal (NCLT) whose main purpose will be to make it easier to liquidate sick companies within a short timeframe of two years. The NCLT will act as the single forum for sick companies, replacing the existing three forums- BIFR, Company Law Board (which works under the Companies Act, 1956 and handles some cases of dispute resolution and compliance) and High Courts (which deal with winding up of companies).

DISINVESTMENT POLICY

The process of selling of government equities in public sector enterprises is known as disinvestment. Disinvestment in India is mainly a tool for public sector reforms and was, at the beginning, motivated by the need for gaining resources for allocations made in the yearly budgets.

As per the recommendations Rangarajan Committee on Disinvestment of PSEs, government launched a programme of disinvestment. However, the first instalment of disinvestment of shares valued at 6480 crore fetched only 3038 crore in 1991-92. The process attracted a lot of criticism. Moreover, instead of raising resources either to strengthen the healthier PSUs or at least to retire the national debt, the government has been looking at extra budgetary support to bridge the deficit.

In order to speed up the process of disinvestment. Government of India set up a separate Department of Disinvestment in March 2000. A decision was also taken to reduce Government?s equity in non-strategic PSUs to 26% or less through strategic sale of such shares. Only three areas-defence, atomic energy and railway-were identified as strategic and all other sectors were open to disinvestment up to 26%.

The then NDA Government pursued this policy of disinvestment and several profit-making PSUs, including IPCL, VSNL and IBP were partially divested. Many state governments were also following similar disinvestment policy in respect of state PSUs.

Disinvestment Policy

· In May 2004, the UPA government adopted national Common Minimum Programme, which outlined the policy of the Government with respect to the Public Sector. It favoured sale of small proportions of Government equity through IPO/FPO without changing the character of PSEs. In regard to this, it approved using of unlisted profitable CPSEs subject to residual equity of the Government remaining atleast 51 % and Government retaining the control of management. It also constituted the formation of the ?National Investment Fund?, where the proceeds from disinvestment of CPSEs would be channelized. 75 % of annual income of NIF would be used to finance selected social sector schemes and the nest 2.5% to meet the capital investment requirements of profitable and revivable CPSEs.

· The objective of the disinvestment policy, approved by the UPA-2 government in 2009, is to develop people?s ownership of Central Public Sector Enterprises to share in their wealth and prosperity while ensuring that Government equity does not fall below 51 % and Government retains the management control.

New Disinvestment Policy

· The Department of Disinvestment has been named as Department of Investment and Public Asset Management (DIPAM) from 14th April, 2016. The BJP-Led NDA government is pursuing disinvestment not to vacate the public sector, but to increase its efficiency. The new disinvestment mantra is to reduce interference allow public sector enterprises to function along commercial principles by granting managerial independence in decision-making such as in appointments.

· The new policy clearly highlights a distinction between privatisation and disinvestment. While sales of equity greater than 50%, may be even 100% is privatisation, any tinkering here and their constitutes disinvestment.

· Objective of DIPAM: Efficient management of centre?s investments in equity including its disinvestment in central public sector undertakings.

· Total disinvestments proceeds in the Current Financial Year is Rs. 23,528.73 crore (as on 30th November 2016)

Infrastructure

Production of goods requires supporting services such as transporting of raw materials and finished goods, institutions for offering credit, energy sources such as coal, oil and electric power, communication facilities and social overheads like health, education and housing. All these supporting structures are collectively known as infrastructure.

Infrastructure is broadly of two types:

· Economic infrastructure is located within the system of production and distribution. Some of these are the transport system, banking system and power.

· Social infrastructure contributes to die production process from outside the system. Some examples are education, training, hospitals and housing.

· Communication system is treated as both social and economic infrastructure as it has a role both within and outside the production process.

Although there has been massive investment in infrastructure in successive five-year plans, India is even now far behind global standards in the matter of infrastructure development.

According to the Global Competitiveness Report, 2015 India?s ranking in terms of Global Competitiveness Index was 55 out of 140 countries.

Different methods needed to attract private investment in infrastructure activities must include simplification and transparency in clearing procedures; creating an independent regulatory framework and unbundling infrastructure projects so that private sectors may be able to chose sub- segments in a project.

Some ongoing government schemes to help in development of infrastructure are: Jawarharlal Nehru National Urban Renewal Mission (JNNURM), National Urban Transport Policy

(2006), National Highways Development Project (NHDP),

Special Accelerated Road development Programme for North East Region (SARDP-NE), Pradhan Mantri Gram Sadak Yojna (PMGSY), etc.

Energy

Energy is the most fundamental input into any production process. Advanced countries of North America and Europe had developed their economies at a time when the cost of energy was very low. Coal was the most important source of energy during the Industrial Revolution. In the 20 century, it was replaced by oil, which was an even cheaper source. When the oil producing countries formed a cartel (OPEC) and increased the price of crude oil from ![]() 2.1 per barrel in 1973 to as much as

2.1 per barrel in 1973 to as much as ![]() 28 per barrel in 1980, it hit the developing countries like India the most.

28 per barrel in 1980, it hit the developing countries like India the most.

Although India has abundant reserves of coal, our development process has not utilised this indigenous source. There is an increasing dependence on oil in the energy sector and immediate steps should be taken to tackle this increasing dependence.

Crude Oil

Our production of crude oil declined over the years. The decline is attributed to unexpected reservoir behaviour and lack of new major discoveries. It is estimated that at the current level of consumption, the recoverable reserves of oil in India (approx. 550 million tonnes) would last for only 20-25 years.

India?s crude oil production increased at highest pace in last four years of 5.6% to 3.193 million tonnes in August 2015.

The oil ministry has estimated India will import 188.23 million tons of crude oil in FY16 at a cost of Rs. 4,72,932 crore, compared to 189.43 million tonnes crude worth Rs. 6,87,416 crore imported in FY15, saving Rs. 2,14,484 crore on fuel bill.

Coal

Coal is the most important indigenous source of energy. The energy derived from coal in India is twice that of energy derived from oil, whereas on the other hand, energy derived from coal is about 30% less than energy derived from oil the world over.

India is today the third largest producer of coal in the world.

Million tonnes

|

State |

Proved |

Indicated |

Inferred |

Total |

|

Total |

1259029 |

142506 |

33149 |

301564 |

|

West Bengal |

13403 |

13022 |

4893 |

31318 |

|

Jharkhand |

41377 |

32780 |

6559 |

80716 |

|

Bihar |

0 |

0 |

160 |

160 |

|

Madhya Pradesh |

10411 |

12382 |

2879 |

25673 |

|

Chhattisgarh |

16052 |

33253 |

3228 |

52533 |

|

Uttar Pradesh |

884 |

178 |

0 |

1062 |

|

Maharashtra |

5667 |

3186 |

2110 |

10964 |

|

Odisha |

27791 |

37873 |

9408 |

75073 |

|

Andhra Pradesh |

9729 |

9670 |

3068 |

22468 |

|

Assam |

465 |

47 |

3 |

515 |

|

Sikkim |

0 |

58 |

43 |

101 |

|

Arunachal Pradesh |

31 |

40 |

19 |

90 |

|

Meghalaya |

89 |

17 |

471 |

576 |

|

Nagaland |

9 |

0 |

307 |

315 |

(Source: Geological Survey of India)

Power

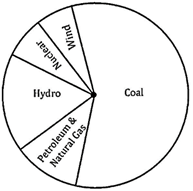

Power has been the most crucial problem in India?s economic development. The share of hydro power is 26%, thermal 66%, renewable energy sources 5% and nuclear 3%. The National Electricity Policy, 2005 recognizes electricity as a ?basic human need? and lays down per capita availability of power from the present 631 units to 1000 units per annum by the end of 2012. In budget 2015, emphasising the need to generate more electricity from clean energy sources, the government announced a massive renewable power production target of 1,75,000 MW in the next seven years. Of the total 1,75,000 MW proposed to be tapped by 2022, solar power will have the major share of 1,00,000 MW followed by 60,000 MW from wind energy, 10,000 MW biomass energy and 5,000 MW of small hydro projects.

A major initiative to expedite power generation has been the development ofcoal-based-Ultra Mega Power Projects (UMPP) each with a capacity of 4000 MW or above. Nine sites have been identified including four pithead sites (Chhattisgarh, Jharkhand, Madhya Pradesh and Odisha) and five coastal sites (Andhra Pradesh, Gujarat, Karnataka, Maharashtra and Tamil Nadu).

The pithead units will get coal from captive mines while the coastal plants will import coal.

Railway

The first train in India was started on a small rail route of 34 kilometers between Bombay and Thane on April 16, 1853. At present, the Indian Railway consists of an extensive network spread over 63974 km comprising Broad Gauge (54257 km) , Meter Gauge (7180 km) and Narrow Gauge (2537 km).With such a large rail route, the Indian

Railway network has become the biggest railway of Asia and the third in the world. Out of this, about 30% of the route kilometre, 41 % of running track kilometre and 43% of total track kilometre has been electrified. Railways absorb about 41% of the total central government employees.

Out of the freight and passenger traffic, the freight segment accounts for about 70% of revenue. Within the freight segment, bulk traffic accounts for nearly 84% of revenue-earning freight traffic (in physical terms), of which about

44% is coal.

The Union Budget 2017-18 has proposed the construction of 3500 km of new rail track and upgrading of select stations.

The government has announced a new metro policy and

Metro Rail Act for standardisation of hardware and software.

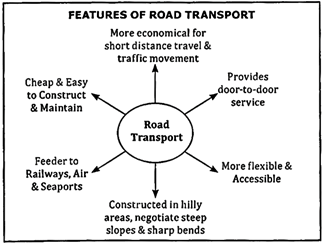

Road Transport

India has one of the largest road networks in the world aggregating to about 3.62 million km at present. A series of initiatives have been undertaken in recent years, to set stage for a quantum leap in India's road system. These initiatives combine new institutional arrangements, highway engineering of international standards, founded on a self-financing revenue model comprising tolls and a cess on fuel. Three initiatives in the road sector were begun in recent years:

The National Highway Development Project (NHDP),

Pradhan Mantri Bharat Jodo Parlyojana (PMBJP), and

Pradhan Mantri Gram Sadak Yogana (PMGSY).

NHDP dealt with building high quality highways. The PNBJP dealt with linking up major cities to the NHDP Highways.

The PMGSY addressed rural roads.

Union Transport Ministry has announced on 4th April 2017 for the construction of the first Express Highway Project of North East in Assam along the banks of Brahmaputra. This, 1300 km long Express Highway Project is likely to incur an investment of Rs. 40,000 crore.

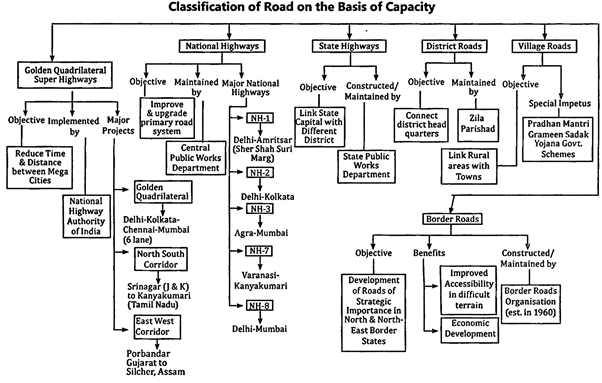

While the Central Sector Programme pertains mainly to National Highways, the responsibility for development of other categories of roads vests with the State/Union territories.

The Indian road network, the second largest in the world consists of 96,260 km of National Highways, 1,31,899 km of State Highways and about 27,17,763 km of Other District and Rural Roads. The National Highways account for about 2% of the total road network but carry as much as 40 % of the total road traffic in the country. Out of the total length of National Highways, 24% is single lane/intermediate lane, 52% is 2-lane standard and balance of 24% is four-lane standard or more.

Union Budget 2017-18 has allocated Rs. 64,000 crore for highway expansion. This is 12% higher than the previous year.

|

Indian Road Network |

|

|

Indian road network of 55 lakh Km. is second largest in the world and consists of: |

|

|

|

Length (In Km) |

|

Expressways |

2000 |

|

National Highways |

100,087 |

|

State Highways |

154,522 |

|

Major District Roads |

2,577,396 |

|

Rural and Other Roads |

2650,577 |

|

Total Length |

55 Lakhs km (Approx) |

Modal shift

· About 65% of freight and 80% passenger traffic is carried by the roads.

· National Highways constitute only about 1.7% of the road network but carry about 40% of the total road traffic.

· Number of vehicles has been growing at an average pace of 10.16% per annum over the last five years.

Inland Waterways

The inland waterways are another mode of transport which was once important but came to be neglected after the development of railways. It is still an important mode in the North-East where almost half of the cargo traffic between Calcutta and Assam is handled by this mode. Total navigable waterways extend to around 14,500 kms of which more than 3700 kms are suited for mechanical crafts. The inland Waterways Authority of India, established in 1986, is entrusted with the responsibility of developing and maintaining national watenvays.

The six existing National Waterways in India

National Waterway 1 (NW1)

The National Waterway No. 1 uses a 1,620-kilometre stretch of the Ganges River. It was declared a national waterway in the year 1986 and runs from Allahabad in Uttar Pradesh to Haldia in West Bengal

National Waterway 2 (NW2)

The National Waterway No. 2 consists of an 891-kilometre stretch on the Brahmaputra River. The waterway was declared on September 1, 1988, and uses the stretch from Dhubri near the Assam-Bangladesh border and Sadiya in North-East Assam.

National Waterway 3 (NW3)

Popularly known as the West Coast Canal, the National Waterway No. 3 is a 168-kilometre stretch that runs from Kollam to Kottapuram in Kerala. The waterway does not follow a specific river. It consists of several canals that form the Kerala Backwaters.

National Waterway 4 (NW4)

The most complex inland waterway, the National Waterway No. 4, was declared on November 24 in 2008.

The waterway consists of the Kakinada-Pondicherry tretch of canals, the Kaluvelly tank, Bhadrachalam-Rajahmundry stretch of River Godavari and the Wazirabad-Vijayawada stretch of River Krishna.

It traverses around 1,095 kilometre from Kakinada in Andhra Pradesh to the Union Territory of Pondicherry.

National Waterway 5 (NW5)

Another waterway with multiple riverlines and rivulets is the National Waterway No. 5. The waterway was declared in November 2008. The NW5 consists of stretches from Talcher to Dhamra on River Brahmani, the Geonkhali-Charbatia stretch of the East Coast Canal, the Charbatia-Dhamra stretch of River Matai and the Mangalgadi-Paradip stretch of River Mahanadi Delta. The waterway also includes a 91 kilometre stretch between Geonkhali and Nasirabad in West Bengal.

National Waterway 6 (NW6)

The last in the list, NW6, is under construction. The waterway is proposed to cover the distance between Lakhipur and Bhanga near the Bangladesh border in Assam, on the Barak River. The first phase of the two-phase project is scheduled to be completed by 2016-17. The waterway aims to benefit people from the northeastern states.

Plans for 106 inland waterways in India

The Union Cabinet, chaired by Prime Minister Narendra

Modi, has approved to pass the official amendment of the

National Waterways Bill, 2015.

Here are some key points you need to know:

· The bill seeks to add 106 inland waterways to the existing six National Waterways on the recommendations of the Parliamentary Standing Committee on Transport, Tourism and Culture and comments of several state governments.

· The bill will also look after the renovation and maintenance of the existing waterways.

· Out of the 106 new waterways, 18 have already been identified. These include five waterways each from Karnataka and Meghalaya, three each from Maharashtra and Kerala, one each from Tamil Nadu and Rajasthan.

· The bill also aims to help the Inland Waterways Authority of India (IWAI) to develop the feasible stretches for Shipping and Navigation.

Shipping

Shipping is another important infrastructure in the country?s trade and industry. Indian overseas fleet ranks the 17 in the world in terms of tonnage, with 659 ships totalling 77 lakh gross registered tonnage (GRT). 102 Indian shipping companies are in operation of which 65 are engaged only in coastal shipping. The public sector Shipping Corporation of India (SCI) has a fleet of 112 vessels aggregating three million GRT.

In spite of this, Indian ships carry only 29% of India's total sea borne trade. More than half of this tonnage is crude oil and its products.

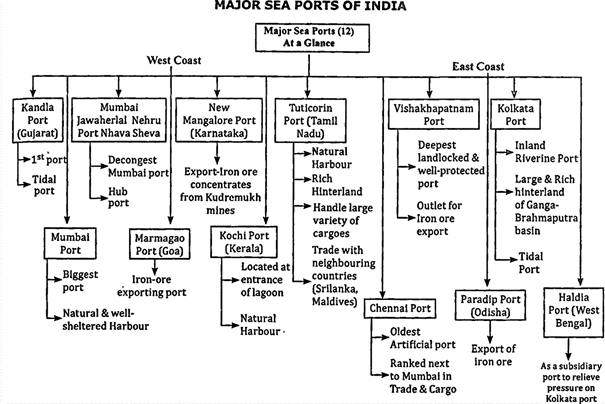

There are twelve major ports under Central Government and139 minor ports under state control along the Indian coastline of about 5600 Kms. The major ports together handle a cargo of 251 million tonnes.

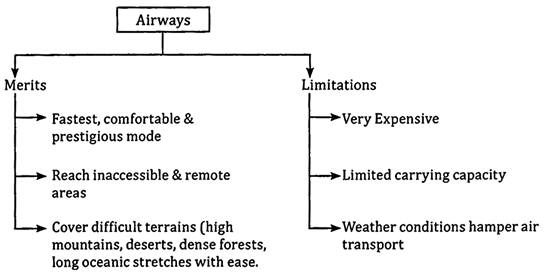

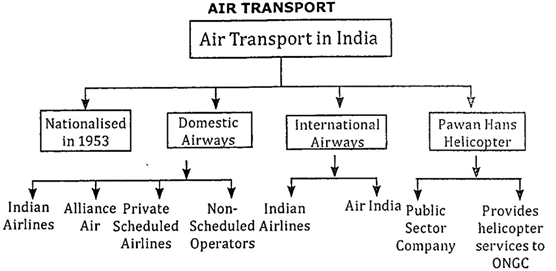

Aviation

Aviation industry

Aviation industry is the highly growing market, in terms of World Economy. It targets to be the third largest market by 2020 and to be in the first position by 2030. Over the next five years, the industry will experience an increase in the domestic and international passenger traffic at an annual average rate of 12 % and 8 % respectively.

Air transport in India made a beginning in 1911 when airmail operation commenced over a little distance of 10 km between Allahabad and Naini. But its real development took place in post-Independent period. The Airport Authority of India is responsible for providing safe, efficient air traffic and aeronautical communication services in the Indian Air Space. The authority manages

125 airports.

Airways

The rapid expansion of this sector during the last five years has necessitated urgent investment in infrastructure. There are 14 scheduled airline operators using 334 aircraft. It is expected that another 250 aircraft will be added during the next five years. In addition, there are 65 non-scheduled airlines operators who have 201 aircraft. The existing airports are unable to manage this increased volume.

The numbers also demand better regulation of the operators in order to ensure satisfactory service. An Airport Economic Regulatory Authority (AERA) was set up to ensure healthy competition among operators and settlement of disputes among operators as well as between them and passengers.

Another major reform in this sector has been the merger of

the Indian Airlines and Air India into a new entity called the National Aviation Company of India Limited (NACIL).

Telecommunication

Telecommunication has witnessed the most dramatic growth since the ending of the monopoly of Department of Telecommunication, as part of the New Telecom Policy of 2012 (NTP 2012)

New Telecom Policy: Highlights

1. Rural Tele-density - To improve rural teledensity from the current level of around 39 to 70 by the year 2017 and 100 by the year 2020.

2. Broadband ? ?Broadband for All? at a minimum download speed of 2 Mbps.

3. Domestic Manufacturing - Making India a global hub.

4. Convergence of Network, Services and Devices.

5. Liberalization of Spectrum - any Service in any Technology.

6. Simplification of Licensing regime - Unified Licensing, delinking of Spectrum from License, Online real time submission and processing.

7. Consumer Focus - Achieve One Nation - Full Mobile Number Portability and work towards One Nation ? Free Roaming.

8. Resale of Services.

9. VOIP - Voice over Internet Protocol.

10. Cloud Computing - Next Generation Network including IPV6.

· The number of telephone subscribers in India increased to 1102.94 million in 31st Oct, 2016. The overall teledensity in India reached 86.25%.

· Central government in its decision made in July 2013 notified the enhancement of foreign direct investment (FDI) in telecom from 74% to 100%.

· As per new norms, FDI up to 49% will continue to be on the automatic route.

· If the FDI limit were to cross 49% then it would require the approval of the Foreign Investment Promotion Board (FIPB).

· By this notification, FIPB is also empowered to note that the investment is not coming from countries of concern or unfriendly entities.

· The guidelines allow foreigners to hold key positions (like Chairman, MD, CEO, etc.) of telecom companies, subject to clearance from the Telecom Ministry on a yearly basis.

Information Technology

The enactment of the Information Technology Act (2000) was a milestone in the development of India's IT industry.

It provided a legal framework for e-commerce and electronic transactions. It also addresses the security needs of privacy, authenticity, integrity and non-repudiation over the Internet.

A study by NASSCOM said that software exports for 2016-

17 would grow between 8-10% to about ![]() 140-141 billion, compared with the 11-16% growth estimate for the fiscal year 2016-17. The Indian domestic market is expected to grow by 14% to

140-141 billion, compared with the 11-16% growth estimate for the fiscal year 2016-17. The Indian domestic market is expected to grow by 14% to![]() 48 billion in the current fiscal year, mainly because of e-commerce growth. Domestic growth is expected to be led by e-commerce, government initiatives and technology adoption by industries. Investment of

48 billion in the current fiscal year, mainly because of e-commerce growth. Domestic growth is expected to be led by e-commerce, government initiatives and technology adoption by industries. Investment of ![]() 26 billion by the government in 2014-15 also helped domestic revenue growth.

26 billion by the government in 2014-15 also helped domestic revenue growth.

The IT industry is the biggest private sector employer in India, and it added 230,000 employees in 2014-15, thus making the total number of jobs in the industry close to 3.5 million. However job growth witnessed a decline in 2015-16 and 2016-17.

The IT sector also accounted for 9.5% of the gross domestic product (GDP). The IT industry holds the largest share of total services exports at 38%.

You need to login to perform this action.

You will be redirected in

3 sec