Answer:

Producer?s equilibrium refers to the state in which a producer earns his maximum profit or minimise its losses. According to MR-MC approach, the producer is at equilibrium, when the Marginal Revenue (MR) is equal to the Martinal Cost (MC) and Martinal Cost curve must on the Marginal Reveneu curve from below:

Two conditions under this approach are:

(i) MR=MC

(ii) MC curve should cut the MR curve from below, or MC should be rising.

MR is the addition to TR from the sale of one more unit of output and MC is the addition to TC for increasing the production by one unit. In order to maximise profits, firms compare its MR with its MC.

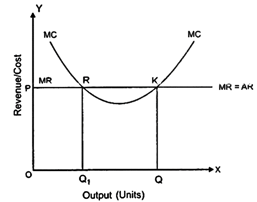

As long as the addition to revenue is greater than the addition to cost. It is profitable for a firm to continue producing more units of output. In the diagram, output is shown on the X-axis and revenue and cost on the Y-axis.

The Marginal Cost (MC) curve is U-shaped and P = MR = AR, is a horizontal line parallel to X-axis.

MC = MR at two points R and K in the diagram, but profits are maximised at point K, corresponding to OQ level of output. Between OQ and OQ levels of output, MR exceeds MC. Therefore, firm will not stop at point R but will continue to produce to take advantage of additional profit. Thus, equilibrium will be at point K, where both the conditions are satisfied.

Situation beyond OQ level.

MR < MC when output level is more than OQ, MR < MC, which implies that firm is making a loss on its last unit of output. Hence, in order to maximise profit a rational producer decreases output as long as MC > MR. Thus, the firm moves towards producing OQ units of output.

You need to login to perform this action.

You will be redirected in

3 sec